Budgets get blown. Audits uncover hidden systems. Non-compliance penalties dwarf what the certification would have cost. Here’s the honest picture.

Every conversation about accepting card payments eventually arrives at the same question:

How much does PCI DSS compliance actually cost?

The internet gives you a range. Online estimates suggest anywhere from a few hundred dollars for a small merchant to tens of thousands for larger organisations, with significant variation by region, merchant level, and which QSA firm you engage. At first glance, that seems helpful.

It rarely is.

In practice, two companies processing similar payment volumes can face dramatically different compliance bills. The difference does not come from transaction numbers. It comes from how payment systems are architected, how cardholder data moves through infrastructure, and most critically, how clearly the cardholder data environment (CDE) is defined before the audit clock starts.

This article breaks down what’s actually driving compliance costs globally, where budgets consistently go wrong, and what the numbers look like once you account for the variables most estimates conveniently ignore.

Why Global Cost Estimates Are Harder Than They Look

PCI DSS is a global standard, but compliance costs are anything but uniform. Four variables account for most of the regional variation.

QSA Location and Regional Fee Structures

Qualified Security Assessors charge substantially different rates depending on where they operate. Firms in the US, Western Europe, and developed Asian markets typically command premium rates. Assessors in emerging markets may offer lower costs, but quality and depth of expertise vary significantly, and the cheapest QSA is rarely the best value when an audit failure or missed scope item costs you six figures to remediate.

What Buyers Need to Understand About QSA Quality

This is the part most compliance guides skip. Price is not a reliable proxy for competence in the QSA market, and buyers who optimise purely on cost frequently pay for it later.

A lower-cost QSA may appear to save money at the point of engagement. But there are several ways this can turn expensive quickly. An assessor without deep infrastructure experience may miss scope gaps during their own review, which does not protect you from gaps discovered by your acquiring bank or card brands later. A QSA unfamiliar with your specific technology stack, cloud environment, or payment architecture may produce a Report on Compliance that is technically valid but strategically shallow, leaving real vulnerabilities unaddressed.

There is also the matter of what the QSA will and will not push back on. More experienced assessors often identify compensating control opportunities or help organisations restructure their CDE to reduce scope, both of which save money over time. Less experienced assessors tend to work through the requirements mechanically, which can result in over-scoping or unnecessary remediation costs.

When evaluating QSA firms, buyers should ask directly: How many Level 1 assessments has your team conducted in the past 12 months? Do your assessors have hands-on infrastructure or penetration testing backgrounds? Can you provide references from organisations with a similar technology stack? A firm that cannot answer these questions clearly is a risk.

On-Site Versus Remote Audits: A Cost Variable That Changes Everything

The increased adoption of remote audits, which was further accelerated after the year 2020, is a permanent addition to the PCI DSS landscape. The guidelines set by the PCI SSC allow for remote audit procedures, and many QSA companies are able to conduct a significant portion of evidence reviews and interviews remotely. However, it is worth noting that the cost of a remote audit is considerably lower than that of an equivalent onsite audit, by as much as 20 to 40 percent. The cost savings are largely due to travel costs, as well as a reduction in the assessor’s time spent on the audit. For companies that have good documentation, a robust change management system, and a cooperative internal team, remote audits can be just as effective but with a significant cost savings.

On-site audits are still necessary or strongly desirable in the following situations: Level 1 assessments in large and/or complex environments may benefit from the presence of the auditor during network walkthroughs and data center walkthroughs. Large organizations with substantial physical infrastructure, e.g., point-of-sale networks in retail or on-premise data centers, are difficult to assess accurately using screen-sharing technology. First-time audits, in which the QSA team must familiarize themselves with an unfamiliar environment, may benefit from an on-site audit.

Practical Advice for Buyers: Don't make on-site vs. remote a binary choice. And don't allow cost to be a deciding factor on its own. Engage with your QSA on how they approach remote audits from a practical perspective. How do they collect information on physical controls? Are there any areas within your environment that absolutely must be on-site? For a mid-sized organization, a hybrid approach is probably right: remote for documentation and interviews, on-site for physical and network validation.

Professional Liability Insurance

This one rarely appears in cost breakdowns, but it matters. QSA firms operating across international jurisdictions carry professional liability insurance that can represent 15 to 30 percent of their overhead, and those costs get passed directly to clients. US-based QSA firms operate in a more litigious environment, which typically means higher insurance premiums and higher audit fees for their clients.

First-Time Audit Complexity

Initial audits are fundamentally different from renewal audits. The first time around, organisations must invest heavily in discovery activities. This includes mapping the systems, data flow analysis, and remediation planning from scratch. Regional differences in infrastructure maturity and security baseline requirements also play a role. Based on the typical engagement data, initial audits tend to be between 30 to 50 percent more QSA hours than renewal audits.

Third-Party Service Provider Chains

Most modern payment environments involve multiple third parties: cloud providers, payment processors, SaaS platforms. Each one requires evidence collection, testing, and security control validation. The more complex the service provider chain, the more time the audit consumes. Organisations with mature third-party risk management programmes absorb this more efficiently than those building it during the audit itself.

Scope Creep: The Budget Risk Nobody Plans For

If there is a single root cause of PCI DSS cost overruns, it is scope creep. Not complexity. Not QSA rates. Not infrastructure age. Incomplete or incorrect understanding of the cardholder data environment is what blows budgets, consistently, across organisations of all sizes.

Research from Scrut (December 2025) puts scope creep alone at 30-50% cost inflation. When combined with poor change impact assessment processes and unclear responsibility matrices with third parties, total overruns regularly reach 50-100% above initial estimates.

The mechanics are straightforward and brutal: systems found outside the originally defined scope during a QSA audit must be brought into compliance immediately. There is no time to plan. Remediation becomes reactive. Costs spike.

The Systems Organisations Miss Most Often

The cardholder data environment is rarely just the obvious payment infrastructure. Systems that consistently surface during audits after the scoping phase include:

• Application logs: frequently store cardholder data temporarily, often unintentionally

• Archived emails: compliance teams are often surprised to find card data in legacy email archives

• Development and test environments: especially where production data copies exist

• Backup and disaster recovery systems: storing cardholder data is storing cardholder data, regardless of the system’s purpose

• Security infrastructure: firewalls, SIEM, IDS/IPS, and antivirus servers that monitor cardholder networks fall into scope

• Domain controllers and key management servers: anything controlling access to cardholder systems is in scope

• VoIP systems: if calls involve payment card numbers, the recording infrastructure is in scope

Real-World Example: Scope Creep at a Mid-Market Retailer

Initial budget: $18,000. Actual cost: $42,000. During the audit, the QSA found POS backup data on a NAS drive connected to the corporate network. The development team had full production data copies in their test environment. Scope expanded from 8 systems to significantly more. The resulting additional QSA time, network segmentation redesign, and encryption implementation added $24,000 in unplanned costs, a 133% overrun on the original budget.

How to Prevent It

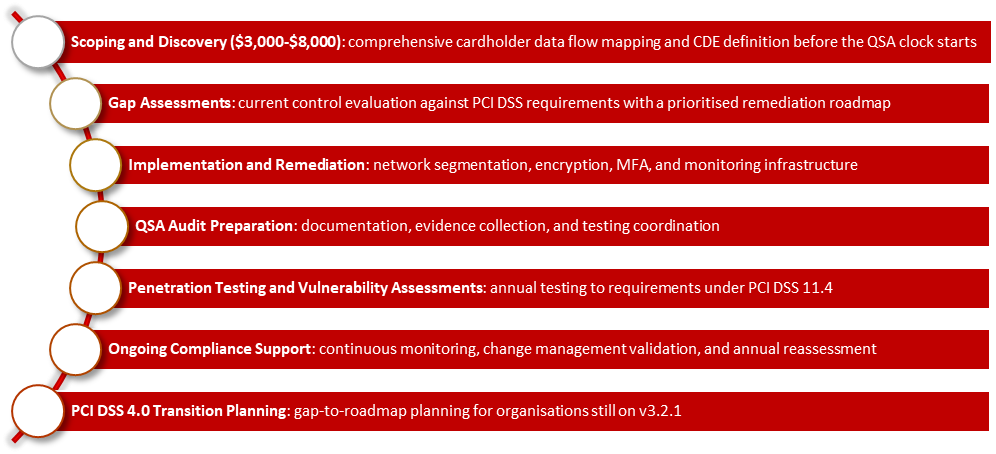

The answer is comprehensive scoping before the QSA audit begins. Not during. Before.

A dedicated pre-audit discovery process should map every system that touches cardholder data, including those that are not obvious to business or IT teams. At RedSecLabs, our scope discovery engagements typically run $3,000 to $8,000 and prevent $12,000 to $25,000+ in audit surprises. The process includes:

• Complete network architecture analysis and cardholder data flow mapping

• Interview-based discovery across IT, development, and business stakeholders

• Automated scanning to surface hidden data repositories

• Third-party service provider assessment and responsibility mapping

• A documented scope statement ready for QSA review

The Real Cost of Non-Compliance

Most organisations focus their attention on compliance audit costs while underweighting non-compliance penalties. This is a material financial error.

Non-compliance penalties escalate. Dramatically. Here’s the penalty structure from Visa, Mastercard, and American Express (2025 schedules):

|

Merchant

Level |

Duration

Non-Compliant |

Monthly

Penalty (USD) |

|

Level 4 |

Months 1-3 |

$5,000 |

|

Level 4 |

Months 4-6 |

$25,000 |

|

Level 4 |

Month 7+ |

$100,000 |

|

Level 1 |

Months 1-3 |

$25,000 |

|

Level 1 |

Months 4-6 |

$100,000 |

|

Level 1 |

Month 7+ |

$100,000+ |

A Worked Example

A Level 1 merchant processing $500M in annual card transactions decides to skip PCI compliance to avoid a $60,000 audit cost. Nine months later, the acquiring bank detects the violation.

Penalties over 9 months using the escalating schedule: approximately $225,000+. Additional card brand fines bring the total to $350,000+ in penalties alone.

If a breach occurs during the non-compliance period, and the risk of breach is exactly what PCI compliance exists to reduce, costs compound rapidly: forensic investigation ($50,000 to $500,000+), customer notification and credit monitoring ($100,000 to $1M+), regulatory fines and litigation ($500,000+).

The Math Is Not Subtle

A $60,000 compliance investment versus $1.2M to $2.5M+ in potential penalties and breach costs. The ROI of compliance is not ambiguous.

What Compliance Actually Costs: Regional Benchmarks

The figures below are extrapolated from global PCI DSS compliance data and regional QSA rate analysis. No publicly available research currently offers region-specific cost studies for PCI DSS compliance, and any source claiming otherwise should be scrutinised carefully. These estimates are directionally useful for budget planning; always obtain quotes from local QSA firms for accurate regional pricing.

United States

|

Merchant

Level |

Typical

Annual Cost (USD) |

|

Level 1 |

$18,000 -

$60,000 |

|

Level 2 |

$6,000 -

$20,000 |

|

Level 3 |

$2,000 -

$10,000 |

|

Level 4 |

$500 - $3,000 |

Western Europe and United Kingdom

|

Merchant

Level |

Typical

Annual Cost (USD Equivalent) |

|

Level 1 |

$15,000 -

$52,000 |

|

Level 2 |

$5,200 -

$17,500 |

|

Level 3 |

$1,700 -

$8,700 |

|

Level 4 |

$430 - $2,600 |

Asia-Pacific

|

Merchant

Level |

Typical

Annual Cost (USD Equivalent) |

|

Level 1 |

$12,000 -

$45,000 |

|

Level 2 |

$4,500 -

$16,000 |

|

Level 3 |

$1,500 -

$7,500 |

|

Level 4 |

$400 - $2,000 |

A note on these ranges: the spread within each band is wide for a reason. Scope size, infrastructure complexity, QSA firm, and geographic location within each region all matter substantially. A Level 2 merchant with a clean, well-scoped environment and good documentation hygiene sits at the low end. One with distributed infrastructure, multiple third parties, and deferred remediation sits at the high end or beyond it.

The Costs That Do Not Show Up in QSA Invoices

Documentation and Training

PCI DSS compliance requires ongoing documentation maintenance and annual staff training. Unlike infrastructure improvements, these are recurring operational expenses:

• Annual security awareness training: $20-$50 per employee. For a 40-person team: $800-$2,000

• Policy and procedure documentation updates: 40-80 hours annually ($2,000-$5,000 in internal labour)

• Network diagram and data flow documentation: 20-40 hours annually ($1,000-$3,000)

Total recurring documentation and training costs: $3,800-$10,000 annually, before QSA or infrastructure costs. Budget this as an operational line item, not a one-time investment.

Mid-Year Change Management

Any change to the cardholder data environment, including new systems, network modifications, cloud migrations, and new payment methods, triggers re-validation requirements. This cost category is almost universally underestimated:

• Network architecture change: QSA re-validation: $2,000-$5,000

• Cloud infrastructure migration: Scope revalidation and new penetration testing: $5,000-$15,000

• New payment method integration: Full scope analysis and testing: $3,000-$10,000

If your organisation regularly modifies infrastructure or adds new payment capabilities, budget an additional 10-15% of annual compliance cost for mid-year validations.

Outsourcing as a Scope Reduction Strategy

One genuinely effective cost lever that is often overlooked: eliminating direct card handling entirely. By outsourcing payment processing to a PCI DSS Level 1 certified processor such as Stripe, PayPal, or Square, you remove the cardholder data environment from your systems entirely.

The trade-off is real: you lose direct control over payment processing and pay per-transaction fees (typically ~2.9%). But for many organisations, particularly at Level 2-4, that fee structure represents a lower total cost of ownership than maintaining in-house compliance infrastructure.

PCI DSS 4.0: The Transition Cost That Is Being Systematically Underestimated

Earlier estimates suggested PCI DSS 4.0 transition would add 10 to 25 percent to compliance costs. Industry data from Protegrity (2025) indicates this is significantly understated, and the ground-level evidence backs that up.

Only 32% of organisations report feeling fully prepared for PCI DSS 4.0. 72% cannot quantify the investment required across people, processes, and technology. That is not a readiness gap. It is a visibility gap, and it is expensive.

Case Study: PCI DSS 4.0 Surprise Costs

A payment processor operating under PCI v3.2.1 budgeted a 10% increase for the 4.0 transition. Actual cost: 38% higher. Unexpected line items included a $45,000 continuous monitoring solution (SIEM), $28,000 in additional penetration testing (expanded scope under 4.0), $18,000 in policy and documentation updates, and $15,000 in staff training. Original budget: $50,000. Actual cost: $156,000.

The key cost drivers in PCI DSS 4.0 transitions:

• Continuous monitoring requirements: typically requires SIEM investment if not already in place

• Enhanced encryption standards: upgrades to existing infrastructure

• Expanded penetration testing scope: more rigorous requirements under Requirement 11.4

• Documentation standards: significantly more stringent than v3.2.1

If your organisation has not yet assessed the gap between your current controls and PCI DSS 4.0 requirements, start now. A gap assessment runs $3,000-$8,000. The cost of discovering those gaps during a formal audit is considerably higher.

How RedSecLabs Approaches PCI DSS Compliance

RedSecLabs is a CREST and QSA certified compliance and penetration testing firm. We work with fintechs, banks, SaaS platforms, and e-commerce businesses to achieve and maintain PCI DSS compliance without the budget surprises that characterise most first-time and transition programmes.

Our PCI DSS service offering covers the full engagement lifecycle:

Start with a free initial consultation. We’ll assess your current compliance posture, surface the likely cost drivers for your specific environment, and give you a realistic roadmap before you commit to anything.

The Numbers That Matter: A Summary

• Compliance costs vary 5-10x: based on architecture and scope. Industry averages are a starting point, not a budget

• Scope creep causes 30-50% cost inflation on its own: pre-audit scoping ($3,000-$8,000) prevents $12,000-$25,000+ in surprises

• Non-compliance penalties dwarf audit costs: a $60,000 compliance investment prevents $1.2M-$2.5M+ in potential exposure

• First-time audits cost 2-4x more than renewals: plan for phased implementation if budget is constrained

• PCI DSS 4.0 transitions cost 20-40% more than v3.2.1 programmes: industry estimates of 10-25% consistently understate real costs

• Outsourcing to Level 1 processors eliminates compliance costs for many smaller merchants: model the total cost of ownership before assuming in-house is cheaper

• Documentation and training are ongoing operating expenses: $3,800-$10,000 annually, not one-time investment.

Start with a Conversation

PCI DSS compliance is not optional if you handle cardholder data. But the gap between a compliance programme that works and one that constantly surprises you is mostly a planning problem, not a budget problem.

If you are approaching a first audit, a 4.0 transition, or simply trying to understand what your environment actually costs to maintain, reach out. The initial consultation is free. For details conatct:

www.redseclabs.com | [email protected]